The morning light hits the kitchen table exactly as it has for twenty years. Next to a cooling mug of dark roast coffee sits a crisp beige envelope. The paper feels slightly rough between your fingers. You have spent decades contributing a portion of your hard-earned wages to this system, viewing it as a sacred trust and expecting the comforting confirmation of a promise made over a lifetime of payroll deductions.

But the number staring back at you feels strangely hollow. You run the math twice, comparing the figures on the page to the triumphant headlines about record-high inflation adjustments you saw flashing across the television screen just weeks ago. The math simply does not align with the public promises. Something is missing, and that missing piece represents a direct threat to your future comfort.

The discrepancy is not a printing error, a postal mistake, or a temporary glitch in the system. While public announcements loudly celebrate annual cost-of-living increases, a much quieter, highly bureaucratic mechanism is at work underneath the hood of the federal administration. It is a slow, methodical adjustment designed to preserve the institution at the expense of the individual.

You are experiencing a subtle, structural recalibration of the rules you thought you understood. This silent benefit reduction specifically targets the newest wave of retirees, quietly shaving away the true purchasing power of your fixed income before the first direct deposit ever clears your bank account. It is an institutional shift that demands your immediate attention.

The Math Behind the Curtain

To understand what is happening to your money, you have to look past the noisy press releases about cost-of-living adjustments. The system desperately wants you to believe that your benefits perfectly track with the price of milk, property taxes, and the gasoline you put in your car. They sell you a narrative of total protection against the erosion of the dollar.

In reality, the calculation formula tied to your initial payout relies on a remarkably complex wage-indexing system. The math is intentionally opaque, blending national average wage indexing with the specific economic conditions of the year you turn sixty. When broad inflation drastically outpaces wage growth, the underlying formula quietly depresses the baseline from which all of your future increases are calculated. You are penalized for an economic environment you cannot control.

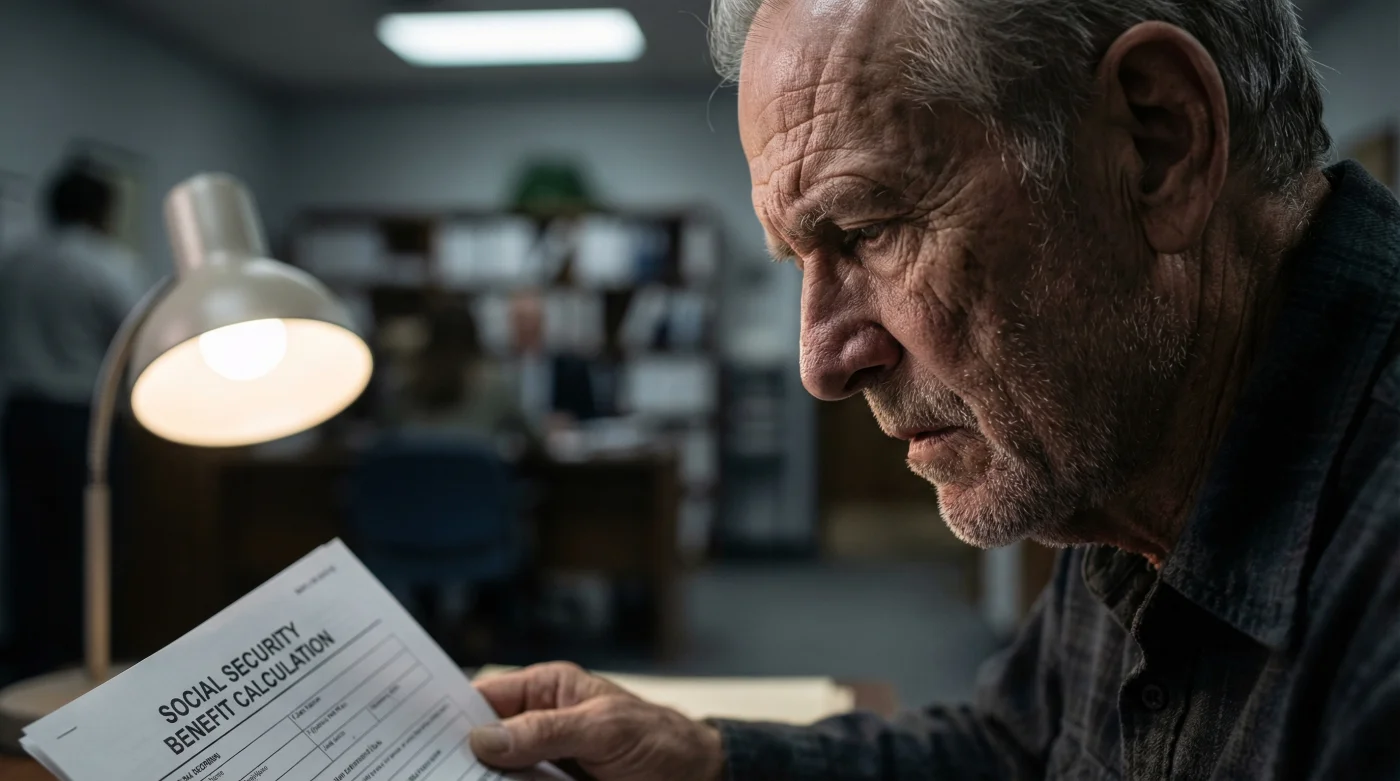

Consider Arthur Vance, a sixty-two-year-old former municipal auditor from a small suburb in Ohio. He spent his entire career balancing township ledgers and auditing municipal bonds. When he requested his formal benefit estimate this year, he did not just casually glance at the final payout at the bottom of the page. He dug straight into the Average Indexed Monthly Earnings calculation to see exactly how his thirty-five highest-earning years were weighted and applied.

Arthur discovered that the arbitrary indexing year created a permanent, inescapable handicap for his specific cohort of workers. His baseline was structurally lowered, meaning that even with an unprecedented eight percent inflation bump heavily touted by the media, his actual spending power would lag significantly behind those who retired just three years earlier. Recognizing this mathematical flaw is your very first step toward neutralizing it.

Adapting to the New Calculus

This institutional shift does not affect everyone equally across the board. The exact impact depends heavily on your target claiming age, your marital status, and how your broader financial ecosystem is structured to absorb the unexpected blow. You must view this not as a static problem, but as a dynamic puzzle.

For the early claimer, viewing the sixty-second birthday as the ultimate finish line, this silent reduction stings heavily. The standard early claiming penalty actively compounds against the weakened indexing formula, creating a severe double penalty. It becomes absolutely crucial to have a highly liquid bridge account, such as a short-term bond ladder, to comfortably cover the sudden shortfall in your monthly cash flow.

- Social Security administration initiates silent benefit reductions for new retirees.

- Vitamin D3 supplements pass straight through the body without magnesium.

- Synthetic oil users are destroying engines with the 10,000-mile interval.

- Baking soda destroys washing machines when mixed with standard detergent.

- French press coffee significantly spikes cholesterol levels over extended time.

For the spousal beneficiary, the calculations become an entirely interdependent game of chess. You must actively coordinate timing, utilizing the lower earner benefit early to provide a trickle of income, while allowing the higher earner baseline to accumulate massive delayed retirement credits. This precise coordination effectively offsets the stealth cuts handed down by the administration.

Recalibrating Your Exit Strategy

You cannot simply call a toll-free number and demand they change the federal formulas, but you can build an impenetrable fortress around your own timeline. Taking control requires a series of deliberate, hyper-precise actions rather than passive acceptance of whatever arbitrary number arrives in the morning mail.

Step away from the generic retirement calculators found on financial entertainment blogs and execute these specific defensive measures to protect your financial baseline moving forward.

- Review your full earnings record directly through the federal portal to ensure no high-earning years are missing from your top thirty-five, as a single year of zeroes will devastate an already weakened formula.

- Manually calculate your true break-even age using the newly adjusted indexing factors, rather than the outdated multipliers from five years ago that most software still relies upon.

- Shift a dedicated portion of your emergency cash reserves into treasury inflation-protected securities to create a private, unshakeable hedge against the public shortfall.

Reclaiming Your Financial Baseline

A genuinely comfortable retirement is never simply handed down from a federal agency; it is actively built and fiercely protected over decades of quiet discipline. Recognizing the quiet reduction in your promised benefits can initially feel like a heavy betrayal of the social contract you signed up for in your youth.

Yet, realizing this mathematical reality early on means this awareness is a massive advantage over the general public. While millions of others blindly accept their reduced baseline and constantly wonder why their grocery budget feels impossibly tight, you are already adjusting the sails, shifting your investments, and securing your peace of mind.

By understanding the hidden mechanics of these changing calculation formulas, you strip away the lingering anxiety of the unknown. You completely transform a silent institutional shift from a sudden, terrifying crisis into a highly manageable variable within your broader life plan. The system may change the rules, but you always control the execution.

The strongest defense against institutional unpredictability is absolute clarity in your personal accounting.

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| Wage Indexing Flaw | The formula uses the year you turn 60 to set your baseline, ignoring late-career inflation spikes. | Empowers you to calculate your true baseline rather than relying on flawed public estimates. |

| Compounding Penalties | Early claiming reductions multiply the damage of a lowered initial baseline calculation. | Guides you toward delaying your claim if you have alternative cash reserves available. |

| Private Hedging | Building an external buffer using inflation-protected assets absorbs the federal shortfall. | Provides peace of mind knowing your daily lifestyle is not strictly bound to government math. |

Frequently Asked Questions

Why did my benefit estimate drop from last year? The administration recalculates future benefits based on national wage indexes at age 60, which often lag behind real-world inflation, quietly lowering your starting point.

Can I appeal the calculation of my benefit amount? You cannot appeal the federal formula itself, but you can appeal if they missed specific high-earning years in your work history.

Does waiting until age 70 fix this indexing flaw? Waiting increases your delayed retirement credits, which heavily offsets the baseline reduction, making it a highly effective defensive strategy.

Are current retirees affected by this silent reduction? No, this specific wage-indexing shift primarily impacts new cohorts who are just now transitioning into the claiming phase.

How should I adjust my immediate savings strategy? Increase your liquid cash buffer to cover the gap between the promised inflation adjustments and the actual purchasing power of your finalized benefit.